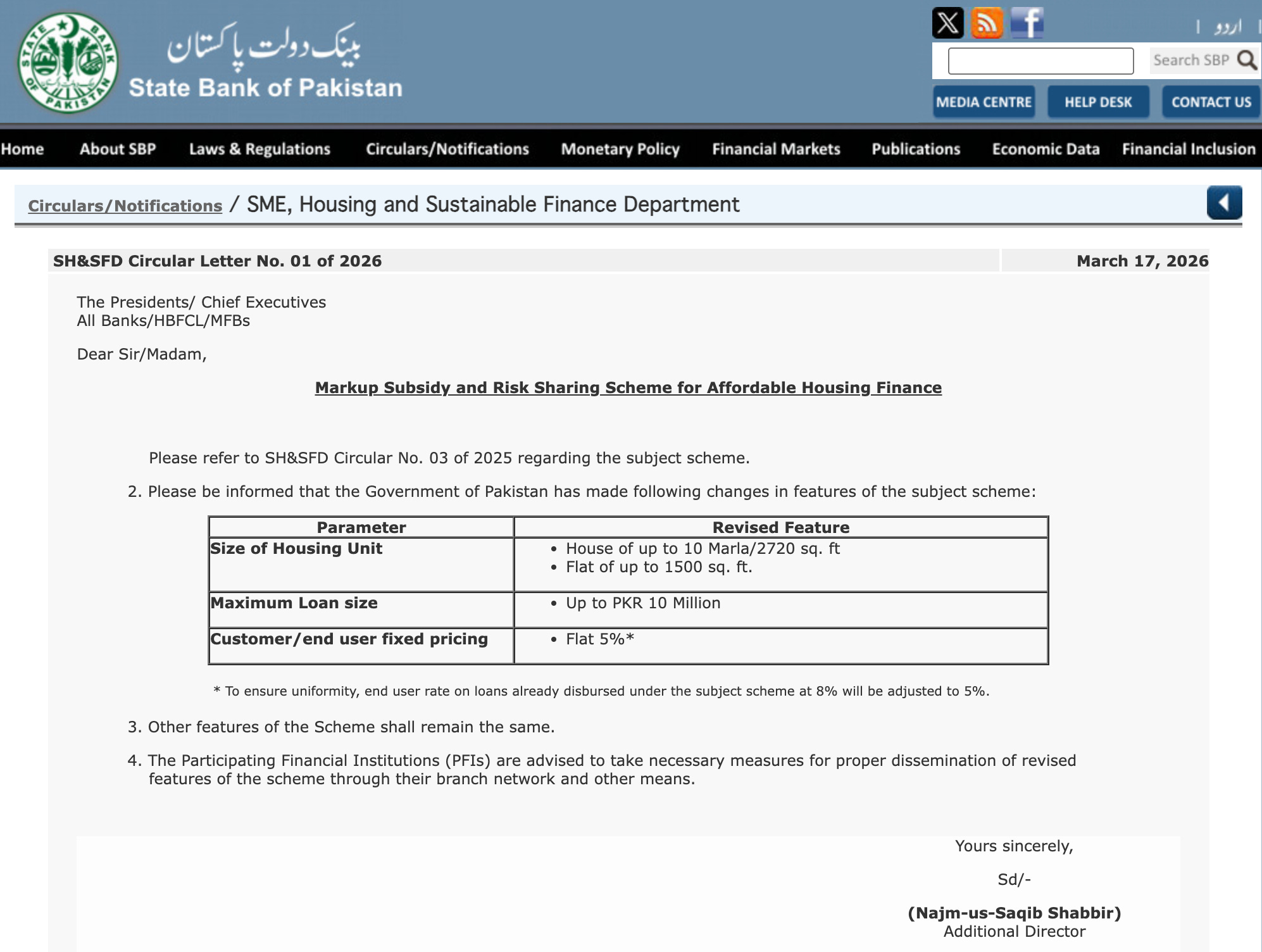

The Five Percent Door

Pakistan's markup subsidy scheme does not solve a housing crisis. It finances one.

Noor Ahmed is forty-four. He lays blocks for boundary walls in Phase 8 of the Defence Housing Authority. He takes the W-11 minibus from Orangi Town at six in the morning and returns after dark. He ha…