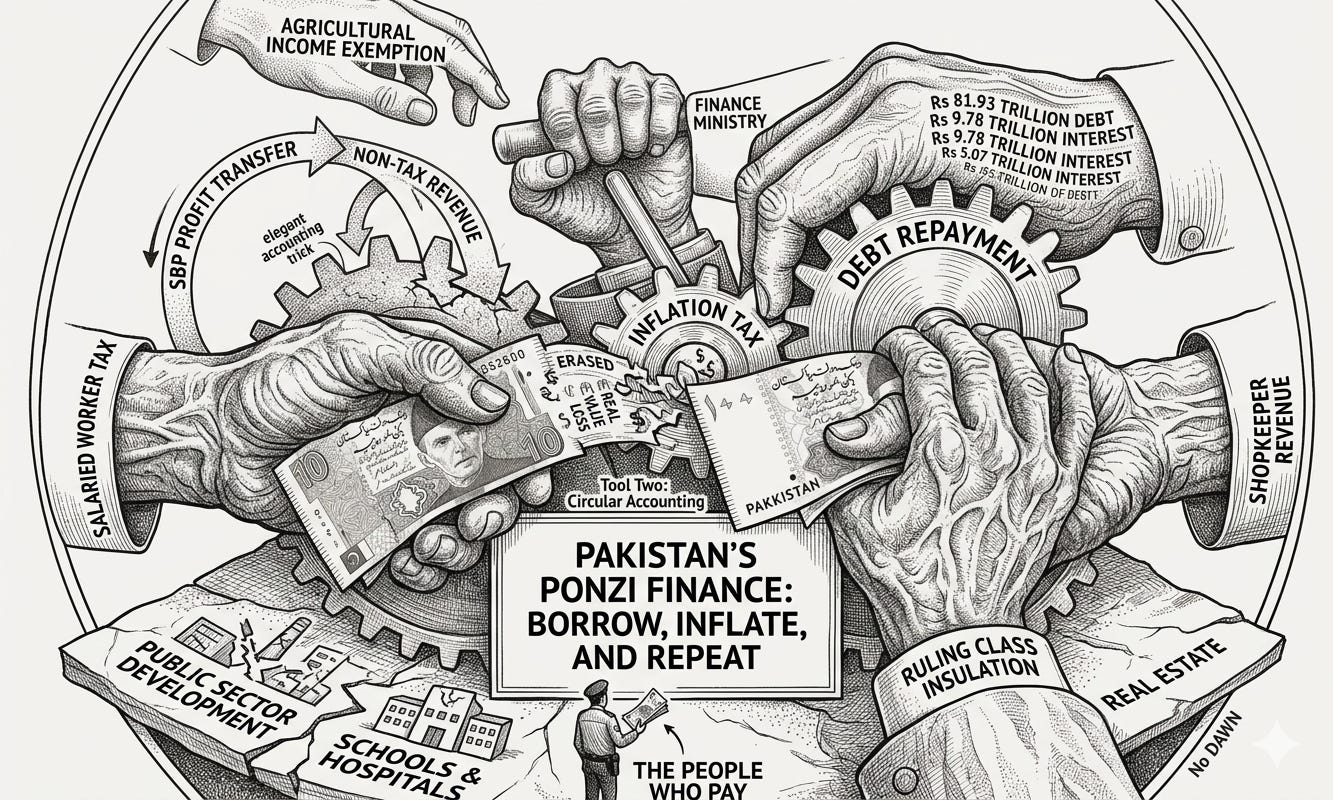

For 25 years the government borrowed to pay its debt, used inflation to quietly erase it, and called the accounting trick revenue. The salaried worker, the shopkeeper, and anyone paid in cash took th…

Continue reading this post for free, courtesy of briefpk.